dynamic

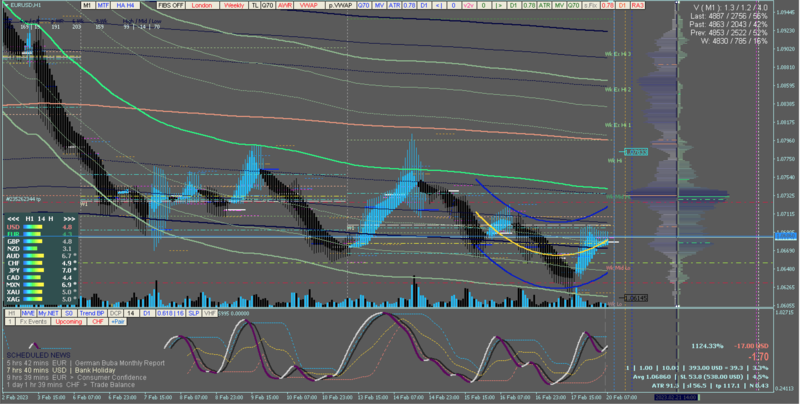

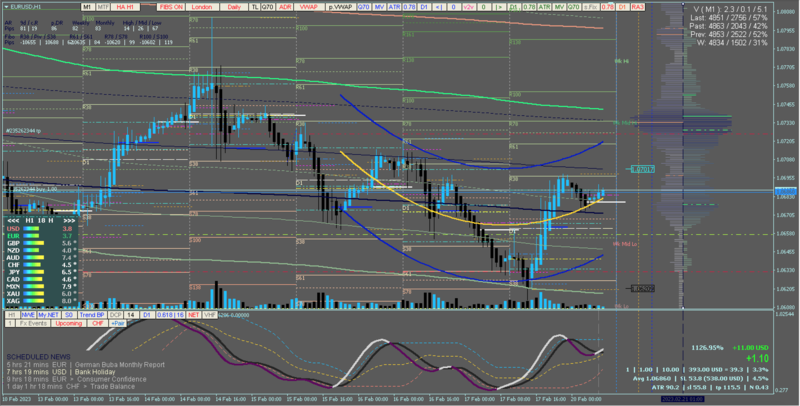

Hurst Exponent with NET

In general, the

Hurst exponent (usually denoted as H) describes the persistence or its lack in the timeseries (e.g., price) behavior. The value of this exponent can be between 0 and 1. If 0 < H < 0.5 for some timeseries, it means that these timeseries are anti-persistent — i.e., a movement in one direction is likely to be followed by a movement in the opposite direction. If 0.5 < H < 1, the timeseries are persistent and the next movement's direction is likely to repeat the previous movement's direction. If H = 0.5 or is very close to it, the timeseries will demonstrate a purely random (Brownian) motion. That is in the ideal world, of course.

Originally, the Hurst exponent was used by Harold Edwin Hurst to predict the Nile floods' levels (you can read more about it in a Wikipedia article.) For traders, the main interest of H is in its alleged ability to show persistence of trends.

Hurst exponent estimation is a viable tool for analyzing the past. Looking at a correctly estimated H value can answer the following question: was the market persistent or was it anti-persistent? In its turn, that would help you analyze performance of your trading strategy or expert advisor during that particular period.

This variation uses the featured technology below for the v2v dynamic trading system...

☛ Dynamic Zones by Leo Zamansky Ph.D. and David Stendahl

The Dynamic Zone indicator can elaborately show how it solves common trading complications. Extreme investing employs the use of oscillators to exploit tradeable trends in the market. This style of investing follows a very simple form of logic: only enter the market when an oscillator has moved far above or below traditional trading levels. However, these indicator-driven systems cannot evolve with the market because they use fixed buy and sell zones. Traders typically use one set of buy and sell zones for a bull market and substantially different zones for a bear market.

Herein lie the complications. Once traders begin introducing their market opinions into trading equations, they negate the system's mechanical nature by changing the zones. The objective is to have a system automatically define its own buy and sell zones and thereby profitably trade in any market -- bull or bear. Dynamic Zones offer

a solution to the complications of fixed buy and sell zones for any indicator-driven system.

☛ My NET ( Noise Elimination Technology )

The My Net is a technical indicator that employs Kendall correlation to remove nonlinear noise. Two main plots are calculated: My(Base) and NET wherein the bases are the following: RSI/RSX, T3-based RSI/RSX, and Elegant Oscillator. Each plot can be used as a confirmation of the other.

My NET is a modified Relative Strength Index, similar to what is used in RocketRSI. It is calculated as the ratio of the sum of recent one-bar close price differences to the sum of absolute values of these differences.

NET is calculated as Kendall correlation of My NET. The NET plot is less noisy than RSI, however, the usage of additional filters may be beneficial.

☛ SmoothStep function... (S0 & S1) fused with dynamic My NET

Returns a value from 0 to 1 that represents a parameter's proportional distance between a minimum and maximum value. The SmoothStep function lets you gradually increase an attribute such as Opacity from 0 to 1, but nonlinearly, over a time range.

Since Frank Sinatra sings in his own way, my charts sing... ♪ I did it, My... Way... ♬ ; )─