Focus: 300,000 German companies face bankruptcy:

"High energy costs, existing supply chain problems and inflation pose challenges for many companies, -Frank Schlein, Managing Director of Crif Germany.

RUSSIA-CHINA ENERGY TRADE

663Breaking Market News  @financialjuice

@financialjuice

9m

RUSSIA’S DEPUTY PM NOVAK: RUSSIA-CHINA ENERGY TRADE TURNOVER UP 64% IN 2022 - RIA.

(Oil cap will go the same way as the gas cap, EU buying Russian oil from the Chinese (or India) at a huge markup. Sanctions

)

)

@financialjuice

@financialjuice9m

RUSSIA’S DEPUTY PM NOVAK: RUSSIA-CHINA ENERGY TRADE TURNOVER UP 64% IN 2022 - RIA.

(Oil cap will go the same way as the gas cap, EU buying Russian oil from the Chinese (or India) at a huge markup. Sanctions

Re: News Ahead

664November 16. The first freight train crossed the Amur railway bridge from Russia to China. The construction of the bridge was implemented within the framework of an agreement concluded between the governments of the Russian Federation and China in 2008.

Re: News Ahead

666For November 21st, 2022, only?

download indicator:

marketprofile_trendlines.mq4

viewtopic.php?p=1295490782#p1295490782

Also check out the pair sentiments over here:

viewtopic.php?p=1295496435#p1295496435

Re: News Ahead

667Upcoming events to the end of year from Pepperstone (Australian Eastern times).

With a quiet week in mind, it also offers a chance to look at the big catalysts left on the calendar that could drive into year-end. I’ve looked solely at the marquee event risks, that matter above all else – these dates need to go in the diary. Arguably all roads lead to a 24-hour window in mid-December, where the ECB, BoE and Fed meet and are expected to hike by 50bp a piece – their guidance and economic projections could set the tone into New Year and into 2023.

30 Nov – EU CPI inflation – this print could decide if we see a 50bp or 75bp hike in the December ECB meeting. The current headline CPI estimate sits at 10.7%, so one questions if we see the estimate move north of 11%.

3 Dec – US non-farm payrolls – we know US payrolls always pose a risk for traders – the Fed want to see a cooling of the labour market, but while we did see a lift in the last unemployment rate report at the last report, the US labour market is still in good health. A US payrolls print below 150k could be taken well by markets, but it’s the unemployment rate (which is taken off the Household Survey) that really drives, so a rise from 3.7% could see risky markets (like equity) rally.

6 Dec – RBA meeting – we should get another 25bp hike, but will we get clearer signs of one more hike in this cycle and then an extended pause? Recall, the RBA doesn’t meet in January, so they’ll refrain from being too explicit and committal here and retain a degree of flexibility.

12 Dec – UK CPI inflation – with UK headline inflation at 11.1%, another rise in price pressures could put the BoE in a real pickle – ever-rising inflation and deteriorating growth are not a great mix for UK assets.

14 Dec – US Nov CPI inflation – after last month’s downside surprise (core CPI came in at 6.3%), sending equity sharply higher and slamming the USD, this CPI print could be huge for markets – one could argue it’s the key data point for the rest of 2022 – should we get another downside surprise and risky asset rally hard into year-end.

15 Dec (06:00 AEDT) – FOMC meeting and Chair Powell presser – the outcome of the Nov US CPI print could influence what we hear from the Fed, but moderation in the pace of hikes to 50bp hike seems very likely – given James Bullard’s comments last week for a terminal rate between 5-7%, we continue to view 5% as the minimum level the Fed is targeting for the fed funds rate, but they’d ideally like to get to a point where the fed funds rate is higher than the inflation rate – so this could be a pivotal meeting, especially given we get new economic and fed funds projections at this meeting and the Fed has made it clear they plan to send a message out, portraying that rates are going higher and will stay high. The market prices the fed funds rate to peak at 5.07% by June.

15 Dec (23:00 AEDT) – BoE meeting – a hard one for the BoE and a clear balancing act – the BoE were dovish at the last meeting, but with very high inflation, and with UK households very sensitive to rate hikes and amid a bleak economic outlook, the BoE are between a rock and a hard place. We should get a 50bp hike here though.

16 Dec (00:15 AEDT) – ECB meeting – the market prices 59bp of hikes here, but while we watch for the ECB to get the deposit rate to neutral there is a focus on how the ECB start to unwind its many asset purchase programs.

With a quiet week in mind, it also offers a chance to look at the big catalysts left on the calendar that could drive into year-end. I’ve looked solely at the marquee event risks, that matter above all else – these dates need to go in the diary. Arguably all roads lead to a 24-hour window in mid-December, where the ECB, BoE and Fed meet and are expected to hike by 50bp a piece – their guidance and economic projections could set the tone into New Year and into 2023.

30 Nov – EU CPI inflation – this print could decide if we see a 50bp or 75bp hike in the December ECB meeting. The current headline CPI estimate sits at 10.7%, so one questions if we see the estimate move north of 11%.

3 Dec – US non-farm payrolls – we know US payrolls always pose a risk for traders – the Fed want to see a cooling of the labour market, but while we did see a lift in the last unemployment rate report at the last report, the US labour market is still in good health. A US payrolls print below 150k could be taken well by markets, but it’s the unemployment rate (which is taken off the Household Survey) that really drives, so a rise from 3.7% could see risky markets (like equity) rally.

6 Dec – RBA meeting – we should get another 25bp hike, but will we get clearer signs of one more hike in this cycle and then an extended pause? Recall, the RBA doesn’t meet in January, so they’ll refrain from being too explicit and committal here and retain a degree of flexibility.

12 Dec – UK CPI inflation – with UK headline inflation at 11.1%, another rise in price pressures could put the BoE in a real pickle – ever-rising inflation and deteriorating growth are not a great mix for UK assets.

14 Dec – US Nov CPI inflation – after last month’s downside surprise (core CPI came in at 6.3%), sending equity sharply higher and slamming the USD, this CPI print could be huge for markets – one could argue it’s the key data point for the rest of 2022 – should we get another downside surprise and risky asset rally hard into year-end.

15 Dec (06:00 AEDT) – FOMC meeting and Chair Powell presser – the outcome of the Nov US CPI print could influence what we hear from the Fed, but moderation in the pace of hikes to 50bp hike seems very likely – given James Bullard’s comments last week for a terminal rate between 5-7%, we continue to view 5% as the minimum level the Fed is targeting for the fed funds rate, but they’d ideally like to get to a point where the fed funds rate is higher than the inflation rate – so this could be a pivotal meeting, especially given we get new economic and fed funds projections at this meeting and the Fed has made it clear they plan to send a message out, portraying that rates are going higher and will stay high. The market prices the fed funds rate to peak at 5.07% by June.

15 Dec (23:00 AEDT) – BoE meeting – a hard one for the BoE and a clear balancing act – the BoE were dovish at the last meeting, but with very high inflation, and with UK households very sensitive to rate hikes and amid a bleak economic outlook, the BoE are between a rock and a hard place. We should get a 50bp hike here though.

16 Dec (00:15 AEDT) – ECB meeting – the market prices 59bp of hikes here, but while we watch for the ECB to get the deposit rate to neutral there is a focus on how the ECB start to unwind its many asset purchase programs.

German energy blackouts

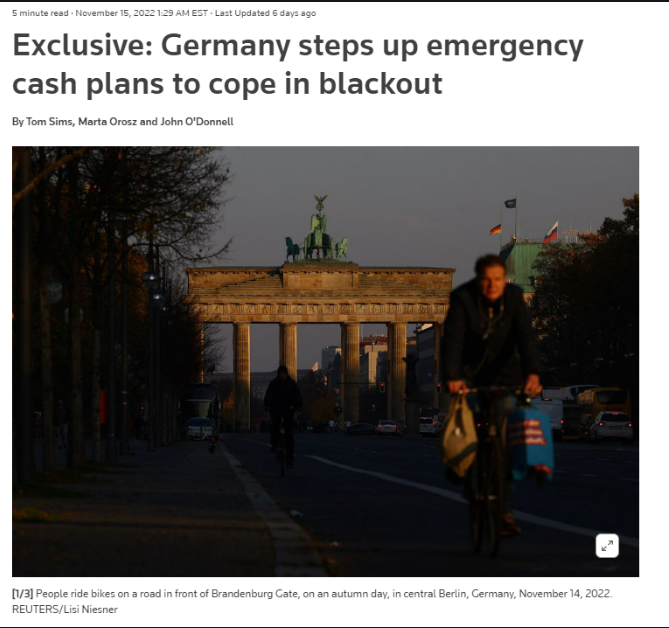

669Germany steps up plans to print cash for energy blackouts.

Lousy energy policies have consequences.

Lousy energy policies have consequences.

- These users thanked the author Ogee for the post:

- Mickey Abi

Re: News Ahead

670Do not show pity: life for life, eye for eye, tooth for tooth, hand for hand, and foot for foot.

Deuteronomy 19:21

Deuteronomy 19:21